译者 王为,来自 市川新田三丁目

Global: Once we are out of this mess, the USD could behammered

by Andreas Steno Larsen

The Fed has delivered new record amounts of USD liquidity, but other channels of USD liquidity remainsubdued. As soon as we approach a reopening of the economy, the USD will likelybe massively hit, with important implications for asset allocation.

美联储投放的美元头寸总量创下新的纪录,但其他渠道提供的美元流动性仍很有限。一旦全球经济接近重启,美元汇率将有可能遭受重击,对资产配置来讲具有重要意义。

The USD has once againproven to be KING in times of crisis, probably asmost debt is still denominated in USDs, which means that USDs are sought after when liquidity tightens globally as has been the case due to the corona lockdowns. TheFed has now acted accordingly via USD swap lines to everyone and their mothers alongside QE in sizes never seen before. USD liquidity is sprayed at every single scarcecorner of the market now. This is ultimately going to kill the USD momentum; itis just a matter of time in our opinion. USD could face a hit of >15% over the coming12-24 months if the global economy gets out of the woods in themeanwhile.

美元再一次证明了自己在危机时期的王者地位,也许是因为大多数的债务仍以美元计价,这就意味着在经济活动因新冠疫情而闭锁引发全球资金流动性收紧之后美元头寸遭到热捧。美联储如今正在按照跟各国央行签署的互换协议向各方提供美元资金,同时以前所未见的力度大搞量化宽松。美元流动性如今正在遍及市场的各个犄角旮旯,美元汇率的上涨动能终将因此而丧失殆尽,我们认为这只是时间早晚的问题。与此同时,如果全球经济在未来12-24个月后脱困成功,美元汇率将难逃下跌15%的命运。

In the following we will try to walkyou through why that is. Upfront you will find our main conclusions:

我们将在下文中致力于探究其中的原因,在此之前先交代几个重要的结论:

I) USD momentum will be halted due tothe massive liquidity injections. USD spot could weaken >10-15% broadlyspeaking.美元汇率的上涨态势会因为美元流动性的大规模注入而夭折,总体上看美元的即期汇率有下跌10-15%的可能;

II) USD hedge costs (versus EUR, NOK,SEK and DKK) will continue to cheapen as $IBOR will likely gradually returntowards zero over the coming quarters.

美元对欧元以及北欧国家货币的汇率的对冲成本将继续下行,因美元LIBOR利率的水平将有可能在未来几个季度里逐步回落至零。

III) The potential outcome space isskewed to the upside for EUR/USD. We find it easier to imagine levels above1.20-1.25 than levels below 1.00, since an even stronger USD from here wouldlikely be met by global coordinated intervention against it – Plaza accordstyle.

欧元/美元未来升值的概率在增加。很容易就可以得出欧元/美元的汇率升至1.20-1.25而不是降至1.00以下的可能性很高的结论,因美元汇率从当前水平继续上涨将有可能遭遇全球如广场协议般的一致干预。

IIII) A new weak USD cycle could beon the cards over the coming 2-3 years, which will have implications for assetallocations. Return on equities in the rest of the world may outpace those seenin the US. It could be time to underweight the US in the allocation strategy.

未来2-3年大概率将进入新的美元贬值周期,这将对资产配置产生潜在的影响。全球其他国家股市的回报率应超过美国股市,当前应考虑在资产配置策略中调降美国股市的投资占比。

Fed: Saving the world with USD liquidity

美联储拿出美元流动性来挽救世界

The Fed has launched USD liquidity programmes for right about everyone in a historic attempt to cheapen the USD in swap markets . The very swift move back to the effective lower bound on the policy rate has cheapened the USD hedge costs materially in recent weeks, despite the USD funding stressthat has been seen in both FX basis and IBOR/OIS spreads.

美联储推出历史性的行动计划面面俱到地向几乎每一个关联方提供美元流动性以降低通过美元互换市场获取美元头寸的成本。美联储在最近几个星期里迅速地将政策性利率的水平调回至历史低位令美元汇率的对冲成本出现了实质性地下降,尽管美元融资紧张的一面在外汇互换点差以及美元LIBOR和隔夜拆借指数掉期的利差水平方面均体现了出来。

Swap lines have been widened so thateg the Riksbank, Bank of Korea and more were added on top of the big CBs that also had a swap line during the financial crisis. Furthermore, the FIMA Repo Facility effectively opens a de facto swap line for all foreign official institutions with a custody account at the Federal Reserve.This is an EM swap line in disguise.

美联储本次签署外汇互换协议的央行范围除了几家在2008年金融危机期间也适用于外汇互换协议的主要央行,还扩大到了瑞典央行、韩国央行。此外,美联储通过FIMA回购融资便利(FIMA指的是外国和国际货币当局)事实上开启了对全部外国政府货币机构的互换操作,这些机构只需在美联储开立一个托管账户即可,这是一种乔装打扮的紧急情况下的互换协议。

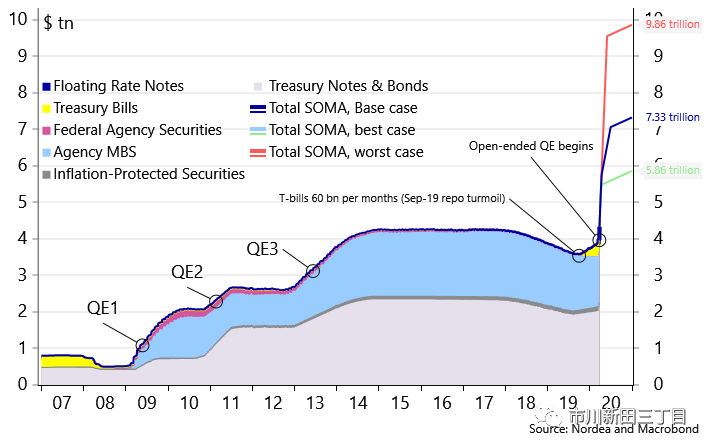

Chart 1: Fed’s SOMA holdings couldeasily double just this year

图1:美联储在公开市场操作账户项下的持仓总量可能很轻易地就将在今年实现翻倍

On top of all the swap lines, the Fed buys bonds at a pace never seen before in an open-ended QE programme, with upto USD 125bn worth of bonds bought PER DAY. These are amounts that would usually not even be seen on a monthly basis. It is not unimaginable that the Fed balance sheet will have more than doubled or even tripled by the end of Q2.Everyone with a need of USDs will get it in size and this should prove to be a game changer for the USD, once we are out of this mess.

除了这些与央行之间签署的外汇互换协议,美联储还通过一个无限额地量化宽松计划以前所未见地力度大笔买进债券,每天的购债规模达到1250亿美元,以前通常一个月也很买不了这么多债。可以想象,联储资产负债表的规模会在2季度结束前翻上一倍甚至涨上两倍。每一个美元头寸的需要方都会得到大量的美元,一旦当前的危机得以解除,这将有可能给美元汇率的走势带来巨大的影响。

USD hedge costs to drop more

美元汇率的对冲成本大幅下行

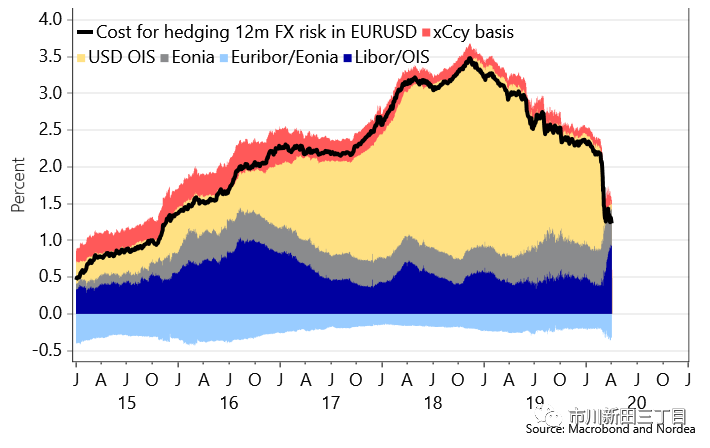

Current 12-month%-costs of hedging USD sales or assets are around 1.25%comparedto almost 2.25% in early February. The Fed has brought the policy rate back tothe 0.00%-0.25% range, which should leave roughly 0.6-0.7% in yearly hedgecosts in EUR/USD as the ultimate target (Fed funds – ECB Deposit), unlessfinancial stress shows up in the FX basis or in the IBOR spreads.

当前为期12个月的对冲美元销售收入或美元资产所面临的汇率风险的交易成本相当于本金的1.25%,而2月初的对冲成本为2.25%左右。美联储已将政策性利率的水平回调至0.00%-0.25%区间。根据欧美政策性利率波动区间最极端的水平来测算,12月期限的欧元/美元汇率的对冲成本约相当于本金的0.6-0.7%,除非外汇互换点差或交叉货币基差互换的实际报价水平体现了金融市场的融资紧张状况。

The $IBOR-OIS spread is the reason why hedge costs have not dropped even more. $IBOR/OIS has widened to >130bpas a result of scarcity of USDs in funding markets. The Fed is now doing whatever it can to alleviate that issue and markets have also priced in a sortof normalisation of $IBOR/OIS for the rest of the year, meaning that over time3-month USD hedge costs will cheapen slowly but surely, if the market is right.

美元LIBOR和美元隔夜拆放指数互换之间的点差是汇率对冲成本没有出现进一步下降的原因。因资金市场上美元头寸严重短缺,美元LIBOR和美元隔夜拆放指数互换之间的点差扩大到了130个基点。美联储正在竭尽所能地解决问题,市场报价也体现出在今年剩下的时间里美元LIBOR和美元隔夜拆放指数互换之间的点差会回归常态的可能性,这就意味着如果市场没看走眼的话,随着时间的推移3个月期限的美元汇率对冲成本将缓慢但切实地出现下行。

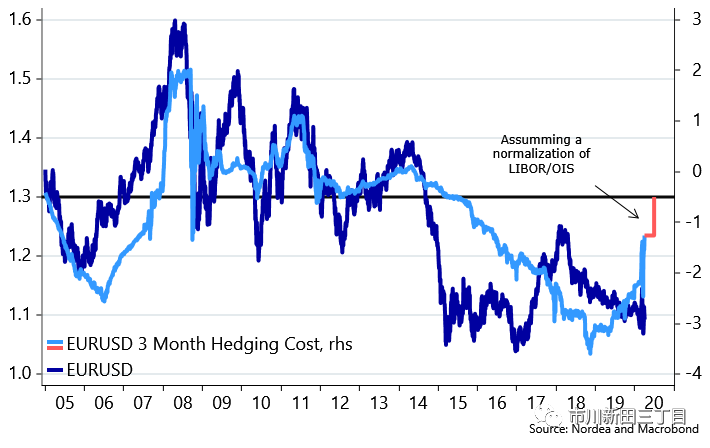

Chart 2: USD hedge costs have fallenoff a cliff, but more could be on the cards

图2:美元汇率对冲成本已经从高位大幅下行,但下跌势头应会继续

If we assume that $-IBOR/OIS normalises over the coming quarter or so, then 3-month USD hedge costs would beback in the ballpark seen prior to the 2013-2014 taper tantrum and oil scare,when EUR/USD traded much higher than today. A simple chart on hedge costsversus EUR/USD spot reveals that >1.25 levels are not impossible,once USD hedge costs have come back towards 0.50%. The Fed is currently doing whatever it takes to cheapen USD hedge costs by providing USDs to everyone and this should also have a spot effect over time.

如果假设美元LIBOR和美元隔夜拆放指数互换之间的点差在未来几个季度里回归常态,3个月期限的美元汇率对冲成本将重回在之前的2013-2014年美联储缩减量化宽松以及油价下跌引发的市场恐慌期间所见过的水平,当时欧元/美元的汇率远高于当前。对欧元/美元即期汇率以及汇率对冲成本进行简单的对比即可知,一旦欧元/美元的汇率对冲成本回到0.5%的水平,欧元/美元的汇率高于1.2500不是没有可能的。美联储正在使尽浑身解数向市场提供美元流通性以降低美元的对冲成本,随着时间的推移这也将产生一些成效。

Chart 3: Normalised FX hedge costs in EUR/USD could lead the pair above >1.20-1.25 over time

图3:欧元/美元汇率对冲成本的正常化应会导致美元汇率升至1.20-1.25区间

USD weakness is coming, we are just waiting for liquidityto rebound in world trade

美元汇率即将出现贬值,只需静候全球贸易的流动性出现上升

When a central bank prints money and widens the monetary base for good, it ought to have a negative effect on the currency. If the Fed prints 4-5trn digital USDs through the rest of the year,it would be an increase of close to 20% of GDP. In comparison the ECB expects to print EURs equivalent to around 10% of GDP. Net/net this should be a USD negative story.

一家央行增加印钞并长期扩张基础货币的总量会给该国货币带来负面影响。如果联储在今年年底之前增加4-5万亿美元的货币总量,该增量将相当于美国GDP的20%,与此形成鲜明对比的是,欧洲央行印钞的规模相当于欧元区GDP总量的约10%。相形之下,对美元汇率构成了利空。

Currently, enough USDs have been printed to lead the DXY index 10% weaker on historical patterns. And this is before accounting for all the money printing that will occur over the coming quarters. The USD probably just needs a green light to weaken from other factors, before this liquidity effect will really kick-in.

当前,美元的发钞量之大足以令美元指数较历史均值出现10%左右的贬值,这还没考虑所有的发钞行为均将在未来几个季度里完成这一因素。美元汇率可能“只欠东风”就会因各种因素的影响而出现贬值,在此之前流动性的影响将成为关键。

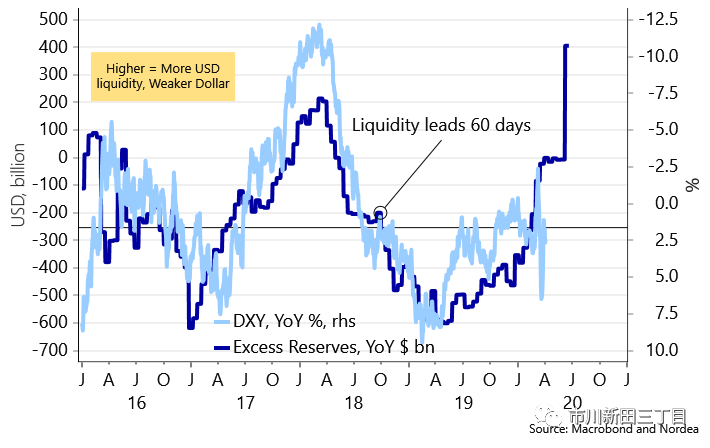

Chart 4: Enough USDs have been printed to weaken the dollar by almost 10% now

图4:美元基础货币的供应量之大足以令美元汇率贬值10%

图中深蓝线代表美元基础货币供应量,坐标位于左轴;浅蓝线代表美元指数,坐标位于右轴,注意数值是倒置过来的,指标向上意味着美元汇率贬值。

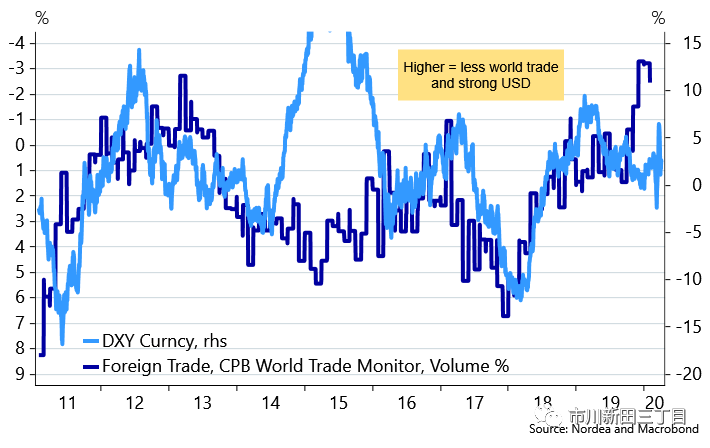

Due to low commodity prices and lessglobal trade, fewer USDs change hands globally and consequently this results ina marked drop in the velocity of USD liquidity, which is one of the reasons whyall these liquidity facilities from the Fed are needed. Usually the USDstrengthens around 10%, when global trade drops 4-5% as we are currentlyseeing. Accordingly, the velocity of USD liquidity will not increase again before the globaltrade rebounds, which is likely a post-lockdown story. Manyplaces are likely to remain locked down for another 4-6 weeks in our view. Oncewe are out of this mess, the USD could be hammered.

由于大宗商品价格下跌以及全球贸易活动减少,全球美元资金的换手率以及美元流动性的流通速率因此出现了明显的下降,这是美联储需要提供美元流动性的诸多理由之一。当全球贸易总量的跌幅达到当前所目睹的4-5%,美元汇率通常会升值约10%。因此,在全球贸易活动出现反弹之前,美元流动性的流通速率将不会回升,全球贸易活动是否会反弹以及反弹程度如何将是居家令解除之后的事情了。我们认为,全球很多地方可能会在未来4-6个月里继续处于闭锁状态。一旦危机得以解除,美元汇率有可能会遭到重创。

In very prolonged curfew scenarios,the USD will likely remain stronger for longer.

如果闭锁状况持续时间非常长,美元汇率将有可能继续走强。

Chart 5: When global trade slows theUSD gains, since fewer USDs will float in the global financial system

图5:当全球贸易活动放缓美元汇率会升值,因全球金融体系中的美元流通量会减少

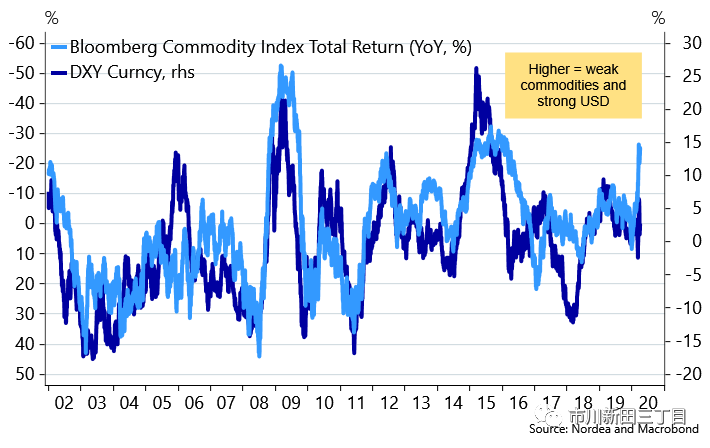

Should the USD lose its momentum andstart a weakening cycle, this would also entail tailwinds for commodities ingeneral. Usually the broad commodity index is a double beta to the DXY index.If the USD weakens 10% then the broad commodity index gains 20%. It is probablynot a bad idea to consider adding long broad commodity positions during thesecond half of 2020.

如果美元汇率失去上涨动力并开始步入贬值周期,从总体上看这有可能会给大宗商品的价格走势带来不利影响。通常大宗商品全指数相对于美元指数的贝塔值为两倍,如果美元汇率贬值10%,那么大宗商品全指数将上涨20%。考虑在2020年下半年加仓做多大宗商品全指数的想法可能并不赖。

Chart 6: Commodities usually gain timestwo, when the USD weakens

美元指数贬值的话,大宗商品价格的涨幅通常是美元跌幅的两倍

A new USD cycle with consequences forasset allocation?

新的美元汇率变动周期如果到来会给资产配置带来何种影响?

A stronger dollargenerally tightens financial conditions outside of the US,which is kind of counterintuitive since that weaker currencies outside of US inprinciple should lead to a competitive advantage. Some mentionable reasons whya strong USD is bad news for growth are that i) EM countries have borrowed inUSD, ii) firms who have borrowed in dollars see debt burdens grow in local currency and iii) thefinancial sector also empirically becomes less keen to lend out when the USD isstrong.

美元汇率走强通常意味着美国以外其他国家的融资状况会出现收紧,这听上去有点不可思议,因为从原理上讲非美元货币相对美元的汇率出现贬值之后应更具有竞争优势才对。至于美元汇率走强为什么会利空经济增长,有一些原因很值得一提:1)新兴国家有大量的美元借款;2)有美元负债的企业以本国货币表示的债务负担出现加剧;3)根据历史经验,当美元汇率走强之时金融行业的对外借款意愿往往会下降。

During recessions ortimes of crisis a strong USD usually builds until aweakening wave takes over. This is exactly what we imagine could happen againthis time around. The trade war and corona crisis respectively worked totighten financial conditions outside of the US alongside the strong USD, andonce the crisis is solved it paves the way for a weakening USD trend.

在经济衰退或危机之时美元汇率通常会先升值然后再来一波贬值,这正是在当前的时点预测将发生的情况。除了美元汇率的升值,贸易战及新冠疫情也分别给美国以外其他国家融资状况的收紧产生了影响,一旦危机得以解除将给美元汇率的贬值打开大门。

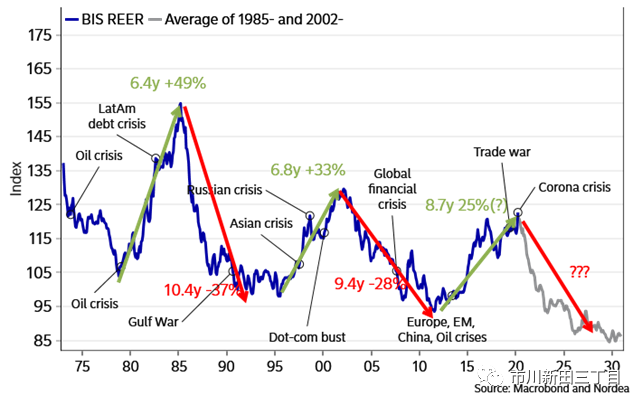

If a new weakening cycle is coming inthe USD, it could prove to be lengthy and material. The two most recent USDweakening cycles led the USD BIS REER index approximately 30% on average over a8-10 year period.

如果美元汇率进入新一轮的贬值周期,其持续的时间将很长,影响将很大。近两轮美元贬值周期的持续时间一般为8-10年,在此期间国际清算银行所公布的美元实际有效汇率指数的跌幅平均为30%左右。

Chart 7: USD cycles from 1970 untiltoday. Usually cycles are lengthy and material

图7:1970年至今的美元汇率变动周期如下,通常每个周期持续的时间会很长,影响会很深远

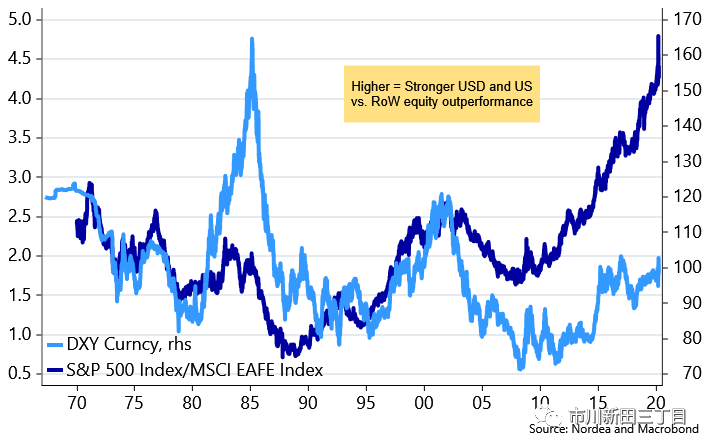

A strong USD usuallyunderpins the return of US equities relative to European or Asian equities,since a strong USD is bad news for financial conditions outside of the US,while the domestically driven US economy usually fares more than OK despite astrong USD.

美元汇率的走强通常会令美国股市的回报表现跑赢欧洲或亚洲地区的股市,因美元汇率的升值对美国以外其他国家的融资状况来讲意味着利空,此外主要靠内部需求拉动为特点的美国经济通常会在美元汇率走强的情况下远比其他国家更具活力。

Hence the direction ofthe dollar is quite important for asset allocation decisions as a new USDweakening cycle could lead to US underperformance versus rest of the world. Duringthe two periods where the dollar showed a long weakening trend, the S&P500underperformed the MSCI EAFE index by 15% (1985 to 1995) and 25% (2002 to2011), while the S&P500 overperformed like crazy during eg the most recentUSD bull cycle. We wrote more about in this piecefrom 2018.

美元汇率的走向对于资产配置的决策关系重大,因新的美元贬值周期有可能会导致美股的表现不及其他国家。在先前美元汇率曾长期处于贬值状态的两个时期里,标准普尔500指数的回报率均落后于明晟北美以外发达国家股市指数,1985至1995年期间的落后幅度为15个百分点,2002至2011年期间则跑输了25个百分点,而在最新一次的美元汇率升值周期里标准普尔500指数的回报率则“激情四射”地跑赢了明晟北美以外发达国家股市指数。我们在2018年的一篇文章中谈到了这一现象。

If the USD cycle turnsnegative, it may make sense to consider underweighting USA alreadywithin the next couple of quarters. We don’t necessarily think that a weak USDis right around the corner due to continued curfews, but 6-12 months out wethink the tide has turned and structurally it is better to position a littletoo early than a little too late.

如果美元汇率转而进入贬值周期,比较靠谱的做法是应考虑在未来几个季度里降低美国股市的投资占比。我们的意思并不是说美元汇率即将因居家状态的持续而立即出现贬值,而是认为如果这种状态持续6-12月,局势将发生结构性的巨变,因此早做准备总比晚做准备要好。

Chart 8: S&P 500 versus MSCI EAFE(Europe, Australasia and Far-East) and the USD. When the USD is strong USequities outperform and vice versa.

图8:标准普尔500指数/明晟北美以外发达国家(欧洲、大洋洲和 远东地区发达国家)股市指数的比率(深蓝线)及美元指数的走势(浅蓝线)对比,美元汇率升值时美股回报率跑赢其他发达国家股市,反之亦然

本站文章欢迎转载,但是必须注明出处“美股投资网meegoo”,并附上本文链接:https://www.meegoo.com/8723.html